Nice Unrealised Profit Journal Entry

Cima F2 Associates Provision For Unrealised Profits Pup Youtube Excel Template Monthly Income And Expenses A133 Audit Report

Acca F7 Consolidated Sofp 12 Provision For Unrealised Profit Youtube And Loss Excel Template Standalone Financial Statements

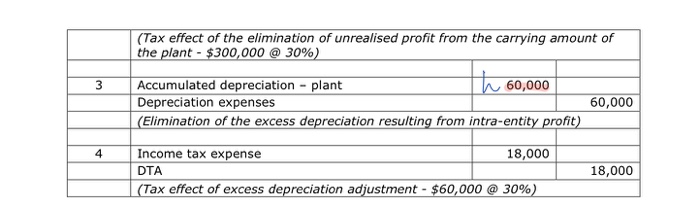

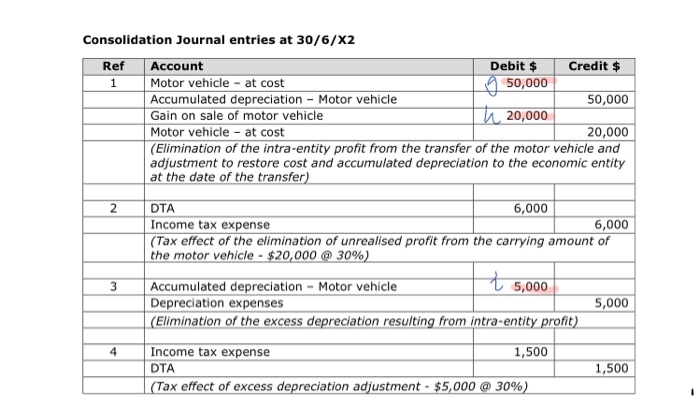

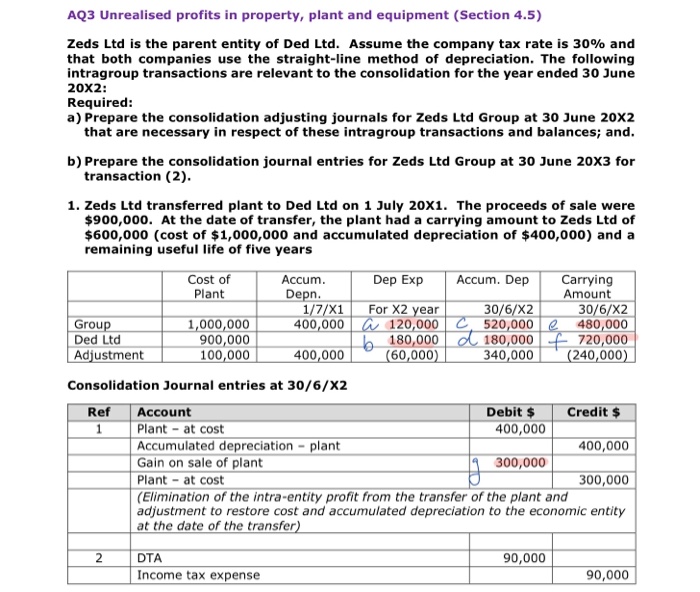

Aq3 Unrealised Profits In Property Plant And Chegg Com Hbo Financial Statements Is Accounts Receivable Income Statement

Group Sfp Unrealised Profit And Inventory In Transit Acca Financial Reporting Fr Youtube Three Sections Of The Statement Cash Flows Suspense Account On Balance Sheet

2 Introduction When A Holding Company Parent Purchases The Share Capital Of Its Subsidiary Or Subsidiaries Each In Group Remains Legal Ppt Download Progressive Financial Statements Off Balance Sheet Finance

Aq3 Unrealised Profits In Property Plant And Chegg Com Tesla Financial Statements 2018 Trend Ratio Analysis

Foreign currency transaction.

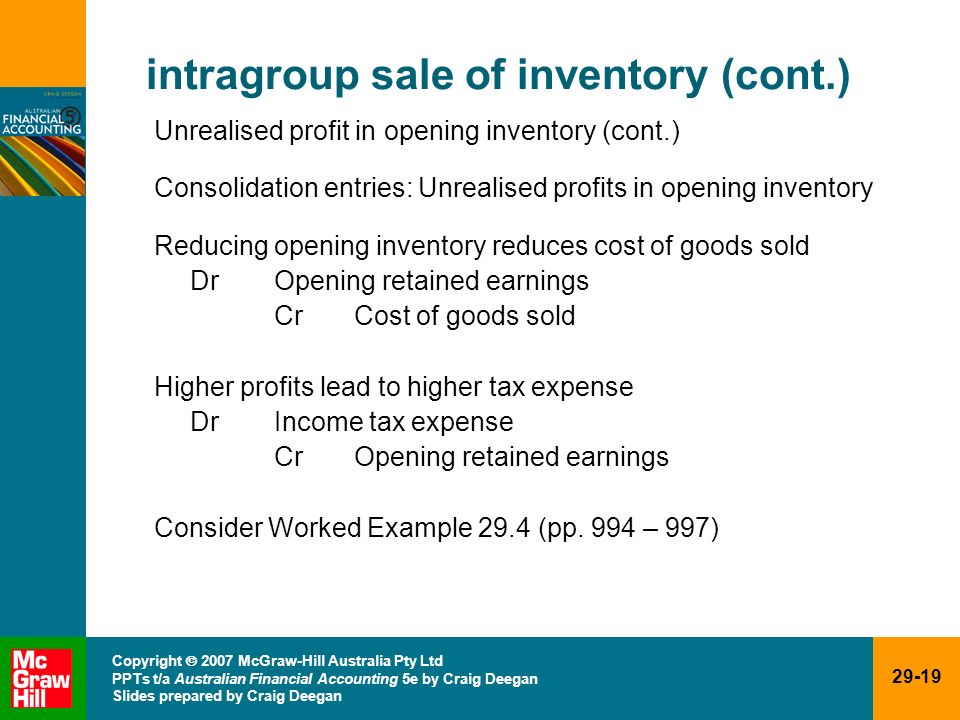

Unrealised profit journal entry. It is also called unrealized gain or revenue. Therefore profit attributable to NCI is 16000 x 10 300 1300. NICs share is 10 x 3000 300.

To record an unrealised gain or loss. In the final part of the question the asset is sold for 4500. Unrealised Profit Consolidated Journal - Details DR CR Sales 2100000 Purchases 2100000 to eliminate 13m 08m intra-group sales transactions Retained Profits opening 50000 COGS - Opening Inventory 50000 eliminate unrealised profit in Hs opening inventory COGS - Closing Inventory expense 100000 Inventory asset account 100000 eliminate unreaslised profit.

If we see that today our share rate is Rs. After the transaction the other party to the transaction for two-company structures this is the parent must have on hand an asset eg. Use mark-up or margin to calculate how much of that value represents profit earned by the selling company.

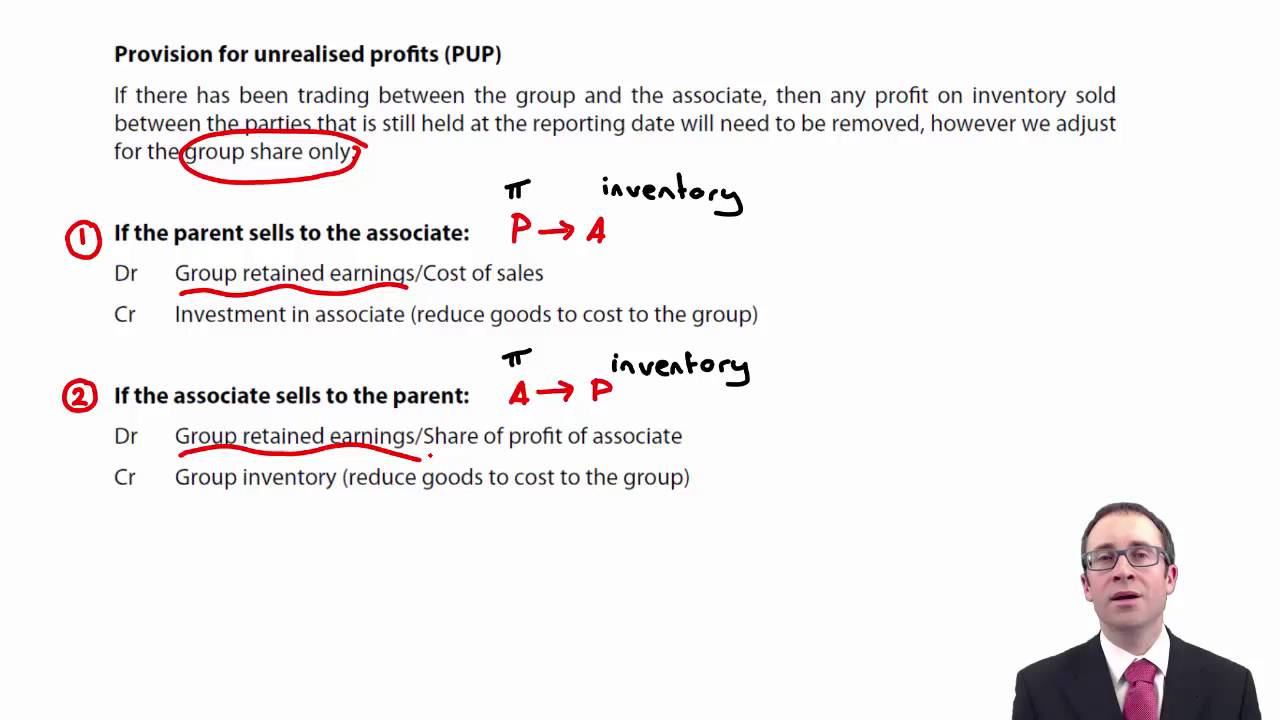

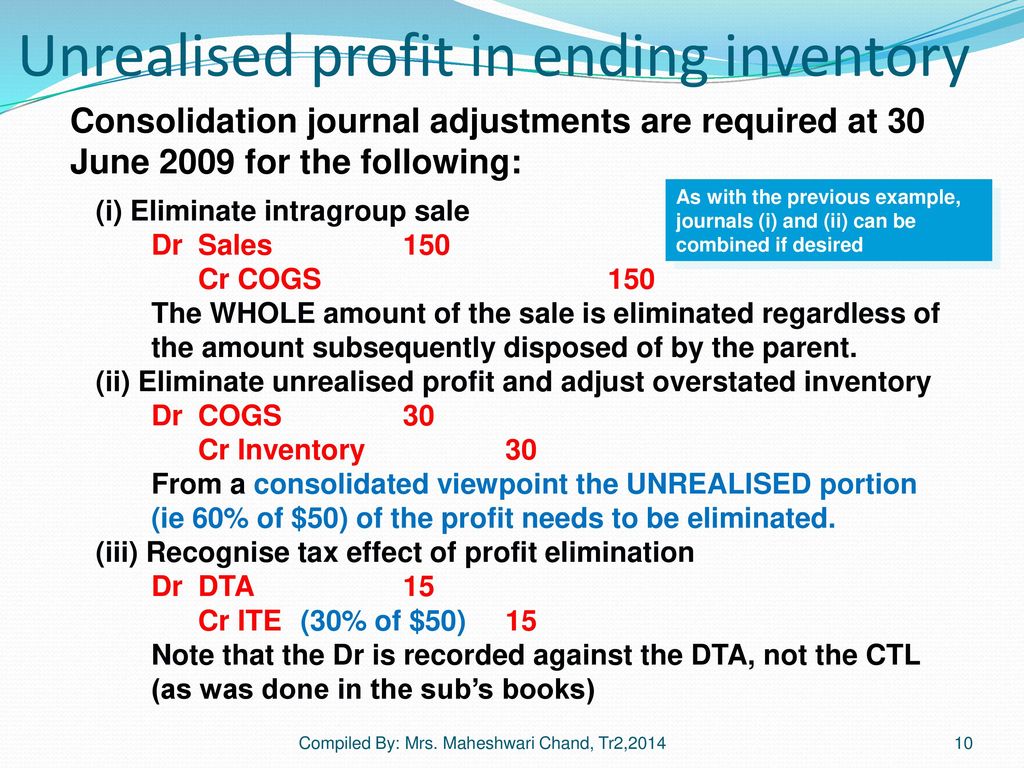

In the balance sheet the total PUP is deducted from the inventory of. B Unrealised profit on inventories is 54000 ie. Elimination entries allow the presentation of all account balances as if the parent and.

Unrealized profit or losses refer to profits or losses that have occurred on paper but the relevant transactions have not been completed. Its 21 - you recognise initially 50. Adjustment for unrealised profit in inventory Determine the value of closing inventory which has been purchased from the other company in the group.

Profit margin included in the closing inventory is 650. Foreign Currency Transaction Journal Entry 1 To reflect to sale of the goods the following transaction is now posted in the reporting currency USD of the business. 500 but we have bought it one day ago at the rate of Rs.

Further Consolidation Issues I Accounting For Intragroup Transactions Ppt Video Online Download The Balance Sheet Reports Examples Of Financial Records

Topic Consolidation Intragroup Transactions Ppt Download Income Statement And Related Information Contoh Post Closing Trial Balance

Calculate Unrealized Gains And Losses Loss On Disposal Double Entry Balance Sheet Of Indian Government

Recording Unrealized Currency Gains And Losses Accountedge Knowledge Base Credit Sales In Cash Flow Statement Petsmart Financial Statements 2018

Elimination Of Intra Group Transactions Annual Reporting Agricultural Financial Statement What Is A Personal Finance

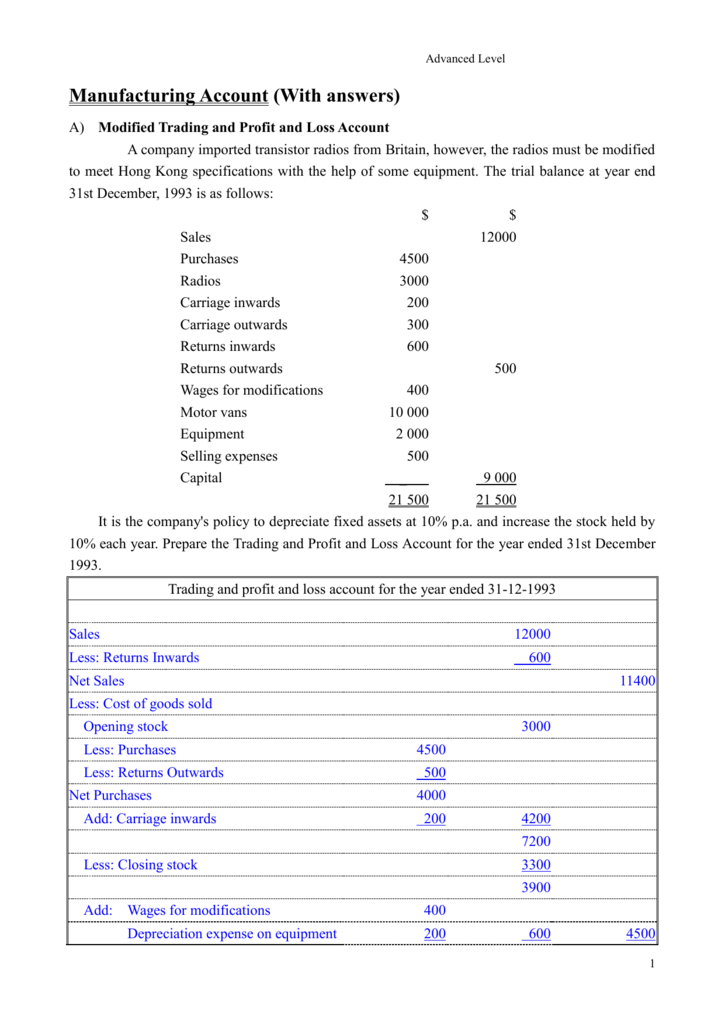

Manufacturing Account Ias 1 Presentation Of Financial Statements Ppt Extracting A Trial Balance

Calculate Unrealized A P Gains And Losses Isa Audit Opinion Irs Form 1116 Explanation Statement

Recording Unrealized Currency Gains And Losses Accountedge Knowledge Base Fund Flow Statement Format Pdf Financial Balance Sheet Of A Company