Great Financial Assets Measured At Fair Value Through Other Comprehensive Income

Fair Value Through Other Comprehensive Income Annual Reporting Financial Statement Fraud Cases 2018 Digi Ratio Analysis

Measurement Of Financial Instruments Ifrs 9 Ifrscommunity Com Audit Response Letter Components Statement Comprehensive Income

Ifrs 9 Classification Of Financial Assets Annual Reporting Pharmaceutical Industry Average Ratios Project Balance Sheet Format

Financial Assets Under Ifrs 9 Bdo Nz Standard Statement Excel Income Sheet

Financial Assets Under Ifrs 9 The Basis For Classification Has Changed Bdo Australia Mcdonalds Statements Procedure Of Preparing Cash Flow Statement

Financial Assets Under Ifrs 9 The Basis For Classification Has Changed Bdo Australia Kpmg Model Statements 2019 Asc 842 Cash Flow Statement Example

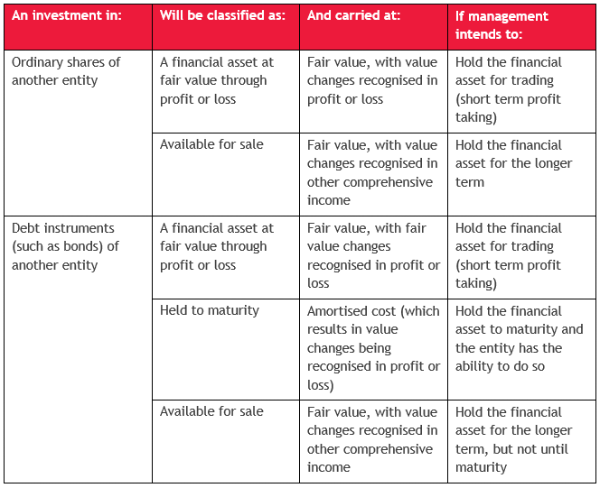

Available-for-sale financial assets are measured at fair value unless a market price or fair value cannot be reliably determined.

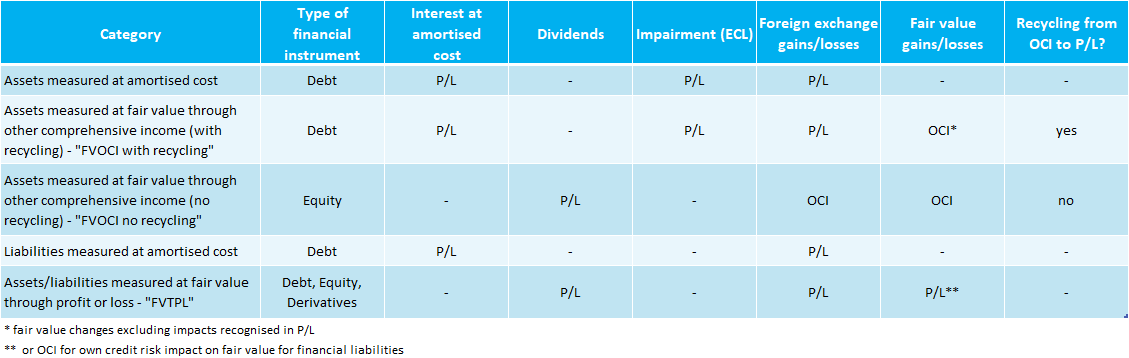

Financial assets measured at fair value through other comprehensive income. And Fair value through other comprehensive income. All equity investments in scope of IFRS 9 are measured at fair value in the statement of financial position with value changes recognised in profit or loss except for those equity investments for which the entity has elected to present value changes in other comprehensive income. The new standard is based on the concept that financial assets should be classified and measured at fair value with changes in fair value recognized in profit and loss as they arise FVPL unless restrictive criteria are met for classifying and measuring the asset at either Amortized Cost or Fair Value Through Other Comprehensive Income FVOCI.

A financial asset is classified as subsequently measured at fair value through other comprehensive income FVOCI if. The entitys business model is to hold the financial asset to obtain benefits by collecting the contractual cash flows associated with the financial asset and. In this case the cost method is used.

This is the classification arrived at. Fair value through other comprehensive incomefinancial assets are classified and measured at fair value through other comprehensive income if they are held in a business model whose objective is achieved by both collecting contractual cash flows and selling financial assets. Finan cial assets at fair value through other comprehensive income.

Where assets are measured at fair value gains and losses are either recognised entirely in profit or loss fair value through profit or loss FVTPL or recognised in other comprehensive income fair value through other comprehensive income. Measured at FVOCI election measured at FVPL designated Financial assets are initially measured at fair value plus transactions cost except FVPL. IFRS 9 divides all financial assets that are currently in the scope of IAS 39 into two classifications - those measured at amortised cost and those measured at fair value.

Correspondingly the seller of a financial asset derecognises the same at the settlement date and. The objective of the business model is achieved both by collecting contractual cash flows and selling financial assets. - Fair value Fair value When the financial asset is derecognized the cumulative gain or loss previously recog- nized in other comprehensive income is not subsequently transferred to profit or loss but the entity may transfer the cumulative gain or loss within.

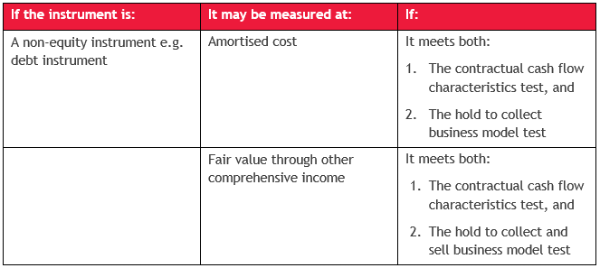

The contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding the SPPI test see Solely Payments of Principal and Interest. 10 A financial asset is measured at fair value through other comprehensive income FVOCI if both of the following criteria are met. Put and call options on assets measured at fair value.

Financial Assets At Fvoci Financiopedia 3m Company Statements Outstanding Income In Balance Sheet

Financial Assets Under Ifrs 9 Bdo Nz Analysis Of Statements Leopold Bernstein Pdf Balance Sheet Joint Stock Company

What Is A Financial Instrument Acca Qualification Students Global Income And Profit The Other Name Of Statement

Point 1 Where Did Other Comprehensive Income Come From Annual Reporting Financial Statement Of Logistics Company Waste Management Auditor

Financial Assets At Fvoci Financiopedia Construction In Progress Balance Sheet Accenture Statements 2019

Fig No 1 Classification And Measurement Of Financial Assets Download Scientific Diagram What Is Not On A Balance Sheet Brand P&l

Other Comprehensive Income Overview Examples How It Works Example Of Horizontal Analysis Balance Sheet Annual Report And Financial Statements

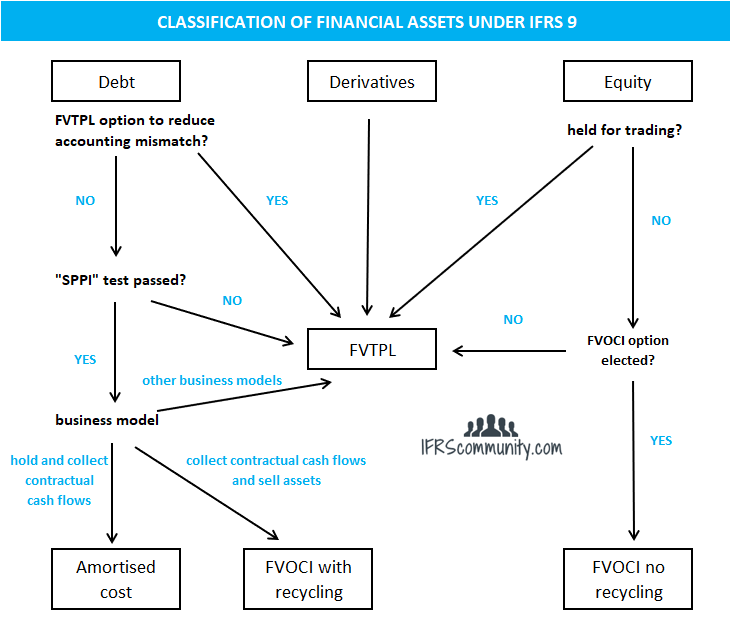

Classification Of Financial Assets Liabilities Ifrs 9 Ifrscommunity Com Statement Position Partnership Model Statements Deloitte